The Trade and Economic Partnership Agreement (TEPA) between the Republic of India and the four European Free Trade Association (EFTA) States—Iceland, Liechtenstein, Norway, and Switzerland—represents a pivotal advancement in India’s trade diplomacy. Signed in March 2024, the landmark agreement is scheduled to enter into force on October 1, 2025. This pact links India, projected to become the world’s third-largest economy, with advanced nations that are global leaders in merchandise and services trade, representing a collective Gross Domestic Product (GDP) of approximately USD 5.4 trillion.

A defining feature that strategically elevates TEPA above conventional Free Trade Agreements (FTAs) is the incorporation of a binding commitment on foreign investment and employment, marking a first for any Indian FTA. The EFTA States have formally pledged to mobilize USD 100 billion of Foreign Direct Investment (FDI) into India over a fifteen-year period, alongside the stated objective of supporting the creation of one million direct jobs. This commitment is monitored via an official investment facilitation mechanism. The mandatory, monitored investment pledge indicates a dedication to long-term economic partnership rather than simple trade volume expansion, signifying EFTA partners’ commitment to anchoring their value chains in India. This strategic positioning supports India’s national initiatives, such as ‘Make in India,’ by encouraging co-production in high-value sectors, including precision manufacturing and clean technologies. This stability is critical for trade strategists, as the longevity of preferential trade access is inherently tied to this FDI commitment, thereby enhancing the reliability of the trade policy environment.

Tariff Liberalization: Scope, Structure, and Schedules

The TEPA provides substantial bilateral market access, though the structure of tariff concessions for goods reflects a balanced approach that protects sensitive domestic Indian sectors.

Market Access Scope and Nuances

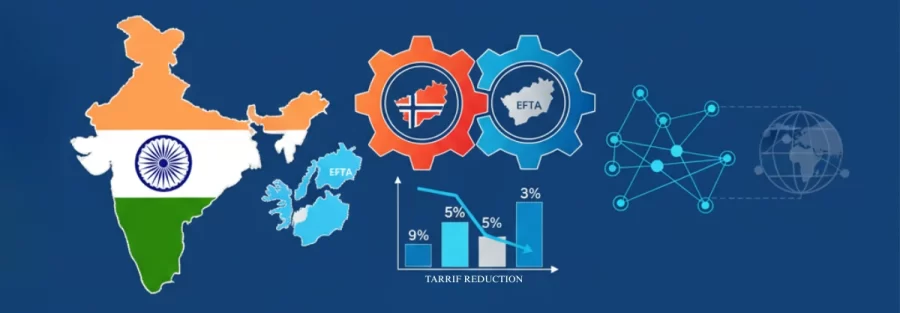

EFTA’s market access offer is extensive, covering 92.2% of its tariff lines, which encompasses 99.6% of India’s existing exports, including the immediate elimination of tariffs on 100% of non-agricultural products and concessions on processed agricultural products (PAP). India reciprocates by opening 82.7% of its tariff lines, covering 95.3% of EFTA exports. However, trade managers must note a crucial nuance: over 80% of EFTA’s existing exports to India consist of Gold, where prevailing duties remain unchanged. This means the liberalization effort is highly targeted toward manufactured and strategic goods.

For Indian importers, understanding the calculation basis for tariff concessions is vital. The agreed-upon Base Rate, the starting point for all tariff reductions, is a cumulative calculation incorporating multiple duty components: the Basic Customs Duty (BCD), the Agriculture Infrastructure and Development Cess (AIDC), the Health Cess, and the Social Welfare Surcharge (SWS).

Decoding India’s Multi-Band Tariff Concession Schedules

India utilizes a granular, multi-band system of tariff elimination and reduction categories designed to strategically manage the opening of its market and protect domestic industrial development. This complexity requires sophisticated compliance tracking systems capable of navigating numerous phase-out periods.

The concession categories defined in India’s schedule include:

- Immediate Elimination (EIF): Duties are removed entirely upon the Entry Into Force date of October 1, 2025.

- Progressive Elimination Categories: Tariffs are phased out gradually over specified periods, categorized as E5 (5 years), E7 (7 years), and E10 (10 years).

- Deferred Elimination Categories: These categories provide a critical buffer period, aligning tariff reduction with strategic policy goals like the Production Linked Incentive (PLI) scheme. Examples include E0 (Eif+5), where duty elimination is immediate but only commences five years after the date of entry into force, or E5 (Eif+5), representing progressive elimination over five years starting five years after EIF. The deployment of these deferred categories ensures that nascent domestic industrial capacity can stabilize production without immediate, disruptive competition from highly efficient EFTA exporters.

- Partial Reduction Categories: Duties are reduced to a fixed residual level rather than eliminated, such as R0 to 2.5% End Duty (immediate reduction to 2.5%) or R5 to 50% (progressive reduction to 50% of the original duty over five years).

| Category Code | Description | Start Date | Elimination Period | End Duty Status |

| EIF | Immediate Elimination | EIF (Oct 1, 2025) | 0 years | Zero |

| E5 | Progressive Elimination | EIF (Oct 1, 2025) | 5 years (gradual elimination) | Zero |

| E0 (Eif+5) | Deferred Elimination (Buffer Period) | 5 years after EIF | Immediate after 5 years | Zero |

| R5 to 2.5% | Progressive Reduction | EIF (Oct 1, 2025) | 5 years | 2.5% |

Sectoral Impacts and Protection

Indian exporters gain improved access in key manufacturing and processing areas, including machinery, organic chemicals, textiles, leather, and processed foods. Pre-FTA tariffs on certain chemical products, which previously reached as high as 54%, will be eliminated, substantially increasing the competitive footprint of Indian chemical products in the EFTA bloc.

Conversely, India has implemented robust safeguards for strategically important and sensitive sectors. These include dairy, soya, coal, medical devices, certain processed foods, and pharmaceutical products, where domestic capacity is being fostered under flagship initiatives. Concessions on these goods fall predominantly under the long, phased reduction schedules (E5, E7, or E10) or partial reduction categories. The reliance on this proliferation of tariff categories prevents the use of simple, static tariff application, mandating sophisticated customs software for accurate, real-time duty calculation.

Rules of Origin (RoO) Mechanics

The Rules of Origin (RoO), detailed in Annex 2.A of the TEPA, are the critical determinant for claiming preferential tariffs. This framework is characterized by flexibility, compliance efficiency, and targeted safeguards.

General Principles and Product Qualification

A product qualifies as originating if it is Wholly Obtained (WO) in one of the Parties, or if non-originating materials have undergone Sufficient Working or Processing (SWP). The SWP criterion is detailed through Product-Specific Rules (PSR) for each HS code, dictating the minimum required transformation. These rules can specify qualification based on Change in Tariff Classification (CTC) or Regional Value Content (RVC), with RVC being calculated using standard methods such as Net Cost or Transaction Value. Importantly, the agreement offers operational flexibility, allowing the PSR requirement to be met by combining operations carried out across different manufacturing facilities within the territory of a single Party.

TEPA’s Advanced RoO Mechanisms

TEPA aligns its RoO with global best practices, such as the Revised Kyoto Convention (RKC) and the WTO Trade Facilitation Agreement, offering features rarely found in India’s previous FTAs.

The pivotal rule for complex supply chains is Diagonal Accumulation. This mechanism allows materials originating in any of the five Parties (India, Iceland, Liechtenstein, Norway, Switzerland) to be considered originating inputs when used in the manufacture of a product in another Party. This facility fundamentally incentivizes complex supply chain integration across the bloc, easing compliance burdens associated with calculating RVC and bolstering the strategic sourcing of high-tech or specialized inputs from EFTA nations.

Furthermore, TEPA incorporates specific trade safeguards, notably the Melt and Pour Rule for iron and steel products. This specific requirement mandates that the fundamental process of melting and pouring the metal must occur entirely within the exporting Party. This non-RVC based rule serves as a powerful safeguard for India’s upstream heavy industry, ensuring that the full transformative process occurs within the free trade zone to prevent trans-shipment of materials originating outside the EFTA bloc.

Administrative burdens are minimized through several facilitative rules, including permission for Accounting Segregation for fungible (interchangeable) materials, simplified inventory tracking for mass-produced goods, allowance for Non-Party Invoicing (Third Party Invoicing), and permissive direct transport rules.

| Mechanism | Definition | Application/Benefit |

| Diagonal Accumulation | Inputs from any of the five Parties (India + EFTA) count towards origin. | Supports multi-national, complex supply chain integration. |

| Melt and Pour Rule | Steel origin requires the core manufacturing (melting/pouring) in the exporting Party. | Acts as a powerful safeguard for Indian heavy industry. |

| Accounting Segregation | Use of inventory methods for fungible inputs without physical separation. | Reduces compliance burden for manufacturers of mass-produced goods. |

Proof of Origin: Certification and Verification Procedures

TEPA adopts the modern concept of “Proof of Origin,” aligning with India’s recent revisions to the Customs (Administration of Rules of Origin under Trade Agreements) Rules (CAROTAR). This flexible approach provides four co-existing pathways for documentation, offering a significant reduction in administrative friction.

Multiple Proof Pathways

To claim preferential tariffs, businesses can use the following documentation:

- EFTA Origin Declaration: A self-declaration completed directly on commercial documents (e.g., invoices) by an Approved Exporter in an EFTA State (for EFTA exports to India).

- Movement Certificate (EUR.1): A traditional certificate issued by EFTA customs authorities or authorized bodies.

- India Agency-Issued Certificate of Origin: Issued by designated Indian authorized agencies, such as the Export Inspection Council or Chambers of Commerce.

- India Exporter Self-Declaration System: Allows approved Indian exporters to self-declare origin.

For high-volume Exim operations, securing Approved Exporter status to utilize the self-declaration system provides a substantial operational premium. This mechanism allows immediate proof generation, eliminating administrative lag associated with agency-issued documents and leading to faster logistics and reduced working capital requirements.

Procedural Requirements and Risk Mitigation

Detailed procedures govern the documentation process. The EFTA-India Certificate of Origin must be issued at the latest within five working days from the date of export. A vital compliance safeguard permits.

Retrospective Issuance in cases of error or involuntary omission, provided it occurs no later than one year from the date of export and is clearly marked “ISSUED RETROSPECTIVELY”. Furthermore, minor discrepancies between the proof of origin and other customs documents, such as typing errors, will not invalidate the origin claim.

A critical procedural requirement for audit preparedness is the Record Retention mandate. Both the issuing authority and the exporter must retain copies of all origin documentation, including supporting manufacturing records, for a minimum period of five years. This lengthy retention period signals that post-clearance verification audits are anticipated.

| Mechanism | Applicable Party | Issuing Body | Time Requirement | Record Retention |

| Agency-Issued Certificate | India Exporter | Authorized Agencies | Within 5 working days of export | 5 years minimum |

| Exporter Self-Declaration | India/EFTA Exporter | Exporter (Approved status required) | At time of export (on invoice/document) | 5 years minimum |

| Retrospective Issuance | Both Parties | Agency or Exporter | Up to 1 year post-export (Must be marked) | 5 years minimum |

Strategic Compliance and Operational Recommendations

Successfully leveraging the TEPA demands proactive operational and strategic adjustments across the supply chain.

Adapting Trade Management Systems

The diverse tariff schedules necessitate immediate system updates. Internal customs software must be configured to integrate the complex classifications (EIF, E5, E0 (Eif+5), etc.) and dynamically calculate the correct duty rate for every relevant HS code for each year following the October 1, 2025, entry into force. Compliance logic must also be validated to ensure the correct cumulative Base Rate components (BCD, AIDC, SWS, etc.) are used when calculating the preferential reduction amount. Failure to correctly manage the deferred elimination categories, where reductions start five years into the agreement, will result in non-compliance.

Maximizing RoO Efficiency

Trade organizations should immediately pursue Approved Exporter status in relevant jurisdictions to capitalize on the reduced friction offered by the self-declaration pathways. Furthermore, supply chain managers must conduct a thorough review of the Bill of Materials (BOM) for strategic products. The diagonal accumulation rule offers a powerful incentive to strategically source materials from any of the five signatory nations to boost Regional Value Content and easily meet complex PSRs.

For manufacturers dealing with iron and steel, strict internal controls and vendor auditing must be instituted to ensure continuous compliance with the stringent Melt and Pour requirement. This requirement mandates deep traceability beyond typical RVC calculation and is non-negotiable for qualifying steel inputs.

Verification and Audit Readiness

Given the five-year record retention rule, trade compliance teams must establish a unified documentation protocol capable of handling all four Proof of Origin pathways. This protocol must ensure that meticulous, auditable records—including RVC calculation sheets, manufacturing records, and purchase orders—are digitized and archived for the full retention period. This readiness is crucial for defending against anticipated post-clearance verification audits. Furthermore, the commitment to specific time-bound verification Service Level Agreements (SLAs) within the TEPA allows for improved risk management, as timely responses by customs authorities are implicitly expected.

The sophisticated compliance requirements under TEPA imply a dual compliance challenge. Teams must be trained on both import protocols (accepting EFTA Origin Declarations) and export protocols (justifying Indian origin) simultaneously, effectively treating India and the four EFTA states as an integrated trade bloc under Annex 2.A rules to achieve maximum utilization benefits. EFTA partners should note that their strategic investment in India directly contributes to fulfilling the binding $100 billion investment commitment, politically reinforcing the stability and duration of the trade concessions.